Document Collection for Condo and Coop Financing

Document collection is one of the most tedious aspects of purchase financing or refinancing a

Financing within the traditional home buying process is simple. When single family home buyers finance the purchase, the lender underwrites them as the borrowers. The home they are purchasing is appraised and becomes collateral, which is secured by the mortgage, protecting the bank. But with condos the process is more complex and borrowers who are financing their purchase need to be aware that their bank has to meet additional requirements not applicable in a single-family home purchase. Why?

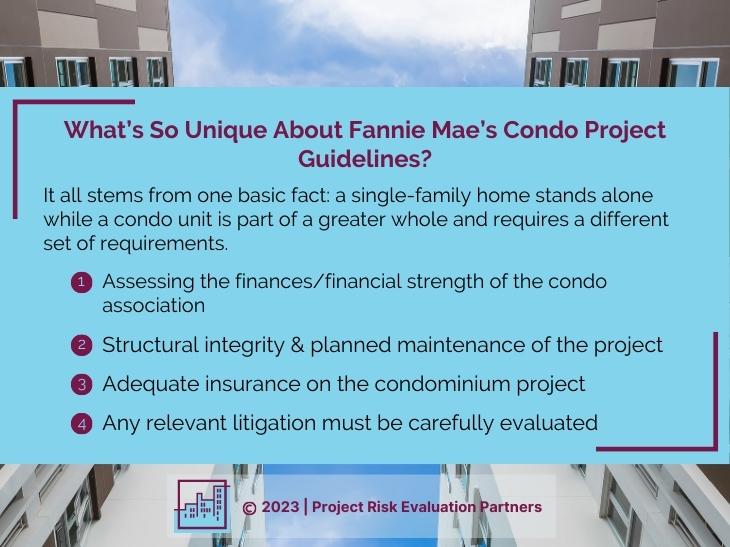

Condos, after all, aren’t quite the same as single-family homes. A single-family home stands alone while a condo unit is part of a larger project. Therefore, Fannie

Mae, which purchases bank loans on the secondary market, has created a unique set of guidelines for purchasing condo loans from banks because a condo unit is one part of a multi-unit project that encompasses common areas, shared amenities, and shared costs. This is why Fannie Mae has lending requirements that are specific to condos. The fact that condos are part of a larger project adds a dimension to the evaluation of the collateral that isn’t there with single-family homes. For condo unit home buyers who are financing their purchase, it is important to understand the basics of these Fannie Mae requirements.

You might be wondering why Fannie Mae is so important to the process of residential lending for condo unit purchases. As a GSE, or Government Sponsored Enterprise, Fannie Mae (shorthand for “Federal National Mortgage Association”) keeps banks in the business of lending! Contrary to what most people believe, banks are not bottomless pits of cash and have a limit to the number of loans that they can issue. Enter Fannie Mae which purchases loans from banks, allowing those banks to issue more loans.

Thus, before purchasing these loans, Fannie Mae’s guidelines and requirements must be met which is called, “project approval.”

It all stems from one basic fact: a single-family home stands alone while a condo unit is part of a greater whole. This single and unique fact requires a different set of requirements. Fannie Mae needs to know that the condominium project meets specific standards as set forth under its guidelines. While Fannie Mae’s guidelines are numerous, extensive, and specific, below are just a few of the complex areas pertaining to Fannie Mae’s guidelines:

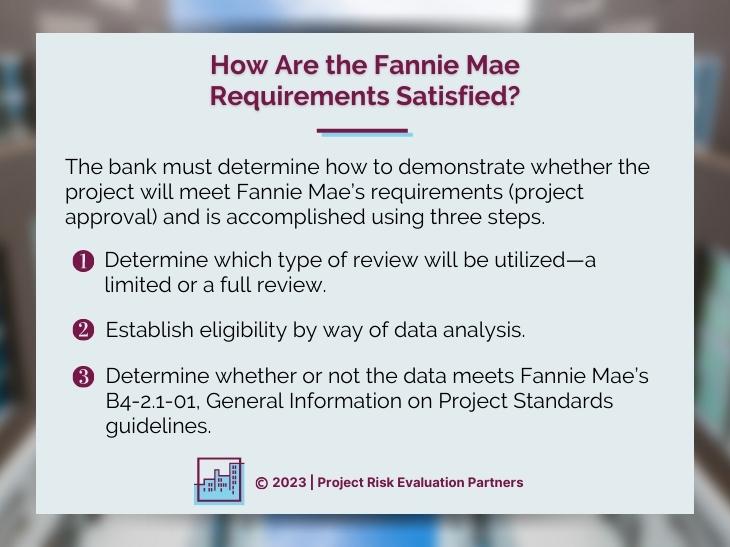

Once a bank begins the process of analyzing the necessary information to undertake a “condo project review,” the bank must then determine how to demonstrate whether the project will meet Fannie Mae’s requirements (project approval). This is done by first determining which type of review will be utilized. Is it going to be a limited review or a full review? Sales and occupancy of condominium units are just two components of determining whether a limited or full review would be appropriate.

Based on whether a limited or full review is necessary, to satisfy Fannie Mae requirements, a bank will then analyze if the project is ineligible which you can read about here.

Once eligibility has been established, the review process includes analyzing data from condo project financial statements, budgets, articles of incorporation, by-laws and other pertinent documents and a determination is made by the bank as to whether or not the data meets Fannie Mae’s B4-2.1-01, General Information on Project Standards guidelines.

Fannie Mae’s condo project approval guidelines are detailed and complex. They need to be. Condominium projects and financing a unit in a condominium project is a more detailed and complex transaction than a single-family home purchase.

Project Risk Evaluation Partners understand the details and the complexity of condo project review and can help you navigate it. Managing client risk is our business so contact us to find out what you need to know.

Document collection is one of the most tedious aspects of purchase financing or refinancing a condo or coop. It is also one of the most

We are thrilled to announce that Project Risk Evaluation Partners was featured in an article by Jennifer White Karp on Brick Underground. The piece, titled “Here’s

Insurance requirements for condos and coops have recently undergone significant changes, with Fannie Mae introducing a new level of detail that requires confirmation of certain

Stay up-to-date with issues important to the Mortgage Industry, Secondary Markets, Residential Lenders, Real Estate Brokers, Condominium and Cooperative Associations Developers, Buyers and Sellers.